Your Guide to a Loan to Help Build Credit

So, what exactly is a loan to help build credit? You might have heard it called a credit-builder loan, and it's a clever financial tool that works a bit backwards compared to a traditional loan. Instead of getting a lump sum of cash upfront, the bank holds the loan amount for you in a locked savings account. You then make small, regular payments over time, and once you've paid it all off, the money is yours.

Your Starting Point for a Stronger Credit Score

Having a low credit score—or no score at all—can feel like hitting a brick wall. Trying to get a car loan, a mortgage, or even a basic credit card is tough when lenders can't see a track record of responsible borrowing. This is exactly where a loan to help build credit comes in. It’s designed to give you a way to create that track record from scratch.

Think of it less like borrowing money to spend and more like a forced savings plan that reports your good behavior to the credit bureaus. It’s a perfect fit for people just starting out, like young adults or recent immigrants, but it’s also a great tool for anyone needing to rebuild after some financial missteps. It's a surprisingly common problem; a 2022 study found that 19% of Americans are "credit invisible," meaning they don't have enough history to even generate a score. This type of loan was practically made for them.

How This Guide Will Help You

Consider this your complete guide to understanding and using these unique loans. We'll walk through everything you need to know, including:

Ultimately, a loan to help build credit puts you in the driver's seat. It gives you a straightforward way to build a positive payment history, which is the single most important piece of your credit score, making up a huge 35% of the FICO score calculation. By the time you're done with this guide, you’ll know exactly how to use one of these loans to build your credit with confidence and open up a world of financial opportunities.

How a Credit-Builder Loan Actually Works

When most of us think of a loan, we picture getting a lump sum of cash upfront. A credit-builder loan, however, flips that script entirely. It's a unique tool designed not for immediate spending, but to prove you can be a reliable borrower—which is exactly what you need to build a strong credit history.

Here’s the breakdown: once you're approved, the lender doesn't just hand you cash. Instead, they place the loan amount, usually somewhere between 300 and 1,000, into a locked savings account or a certificate of deposit (CD). You can’t touch that money. Your job is to make small, fixed monthly payments over a specific period, typically 6 to 24 months.

It's almost like you're paying yourself in installments. Each payment you make is a signal of your financial discipline, and—this is the critical part—the lender reports every single one to the three major credit bureaus (Experian, Equifax, and TransUnion).

The Reporting Process Explained

That reporting is where the real magic happens. As you make consistent, on-time payments, you're actively creating a positive track record on your credit file. This is a huge deal because your payment history is the single most important ingredient in your credit score, making up a massive 35% of your FICO® Score.

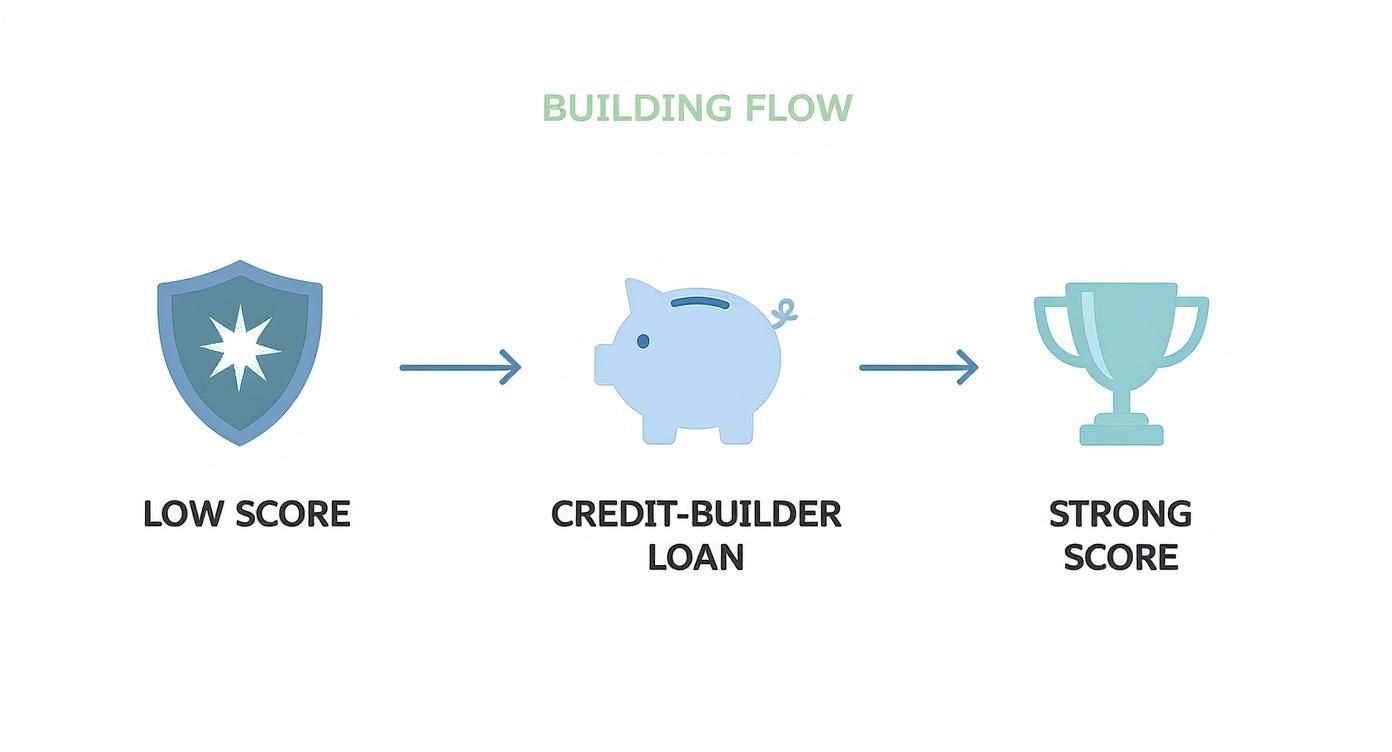

This simple infographic illustrates just how powerful this journey can be, turning a low score into a strong one through these disciplined steps.

It’s a structured path designed to transform a tough starting point into a successful financial future, one small payment at a time.

To really see how different this is from a standard loan, let's put them side-by-side.

Credit-Builder Loan vs. Traditional Personal Loan

As you can see, these two loan types serve completely different functions. While one gives you immediate cash, the other gives you an opportunity to build a stronger financial foundation for the future.

The Final Step: Unlocking Your Funds

Once you’ve made that final payment and completed the loan term, the lender releases the funds from the locked account and gives them to you. Often, you’ll even get a little bit of interest that the account earned along the way. You not only walk away with a better credit score but also a nice chunk of savings you built for yourself.

This one-two punch of credit building and forced savings is what makes these loans so effective. It’s not just a theory; the results are real. Borrowers who use these loans responsibly often see a noticeable jump in their credit scores—some see an increase of up to 60 points once the loan is reported.

On top of that, a credit-builder loan adds an installment loan to your credit history, which helps diversify your credit mix—another small but important factor in your score. By completing the loan from start to finish, you're sending a clear message to future lenders: you know how to manage debt.

The Payoffs of a Credit-Builder Loan

Sure, the main goal of getting a loan to help build credit is to see that score go up. But the benefits run much deeper than just a three-digit number. Think of it less as a simple loan and more as a financial training program that pays you back at the end.

Right off the bat, you start building the single most important part of your credit history: your payment record. Since on-time payments make up a whopping 35% of your FICO® Score, every single payment you make on this loan sends a powerful signal to the credit bureaus. You're proving, month after month, that you’re a reliable borrower, which is exactly what future lenders want to see.

It's More Than Just the Score

Building a solid payment history is a huge win, but a credit-builder loan works its magic in other ways, too. It adds a different type of credit to your report, which helps with your credit mix—a factor that accounts for 10% of your score.

Lenders get a more complete picture when they see you can handle different kinds of debt. If all you have is a credit card (revolving credit), adding an installment loan like this one shows you can manage fixed payments over a set period. It rounds out your financial resume, making you look like a more seasoned and trustworthy borrower.

This little trick acts as a forced savings plan. For many people, this is the first time they’ve been able to sock away a few hundred dollars. Suddenly, you have a small emergency fund or a head start on a bigger goal. It’s this two-for-one deal—building credit while you save—that makes these loans so powerful.

How a Better Score Changes Your Real Life

These improvements to your credit report aren't just abstract points. They translate into real-world advantages that can save you a ton of money and stress. A stronger credit profile opens doors that might have been locked before.

Here’s what that actually looks like:

At the end of the day, a loan to help build credit is a direct investment in your financial future. It’s a low-risk, structured path to prove you’re creditworthy, build up some savings, and unlock the kind of opportunities that only a good credit score can provide.

How to Find and Apply for the Right Loan

So, you're sold on the idea of a loan to help build credit. Great! The next question is, where do you find the right one for you? Thankfully, these loans are becoming more common and are offered by a range of financial institutions that want to help people like you get a solid start.

Where to Look for Credit-Builder Loans

Your best first stop is often close to home: local credit unions and community banks. These places tend to be deeply invested in their communities and often provide better terms, like lower interest rates and minimal fees. Credit unions, in particular, are famous for their member-first philosophy. To get a better sense of what they offer, check out our guide on how to get a credit-builder loan through a credit union: https://www.itinscore.com/blog/credit-builder-loan-credit-union/

Beyond traditional banks, online lenders and fintech companies have jumped into the game, creating a ton of new options. The private credit market has absolutely exploded, growing to an estimated $1.5 trillion at the start of 2024. This boom means more choices for people looking to build their credit history outside the old-school banking system. If you want to see what's out there, you can explore potential credit-building solutions from various providers.

Comparing Your Loan Options

Here’s the thing: not all credit-builder loans are the same. As you start looking around, it pays to be a bit picky. Think of it as choosing a partner for your credit-building journey—you want one that will actually help you succeed.

Here’s a quick checklist to use when you compare lenders:

The Simple Application Process

Worried about applying? Don't be. Getting a credit-builder loan is usually much simpler than applying for a traditional car loan or mortgage. Lenders know you probably don't have a long credit history—that’s why you’re there!

Instead, they'll focus on other things to see if you're a good candidate. You'll typically just need to show proof of who you are and that you have a steady income. This tells the lender you have the means to make the payments. The application is often just a quick online form, and you might get approved in no time. They’re looking for reliability, not a perfect credit score, which makes this an amazing first step for anyone starting their credit journey.

Strategies to Maximize Your Credit Score Growth

Getting a credit-builder loan is a fantastic start, but how you handle it from here is what truly moves the needle. To make sure your efforts pay off, you need to be strategic. Think of it less as just another bill and more as an active tool for your financial future. Let's walk through how to turn this opportunity into real, measurable growth for your credit score.

If there's one golden rule, it's this: make every single payment on time. No exceptions. Your payment history is the heavyweight champion of credit score factors, making up a massive 35% of your FICO® Score. A single late payment can knock you back months, undoing all your consistent, hard work.

The easiest way to guarantee you never slip up? Set up automatic payments the day you open the account. It's a simple, set-it-and-forget-it move that ensures a steady flow of positive payment history gets sent to the credit bureaus.

Amplify Your Efforts with Smart Pairings

While your credit-builder loan is doing its job, you can actually speed up your progress by adding another tool to your kit. Pairing your loan with another credit-building product is a powerful way to diversify your credit mix and feed more positive information into your report.

A great option to consider is a secured credit card. It works a lot like your loan—you put down a small cash deposit as collateral, which makes getting approved much easier. Once you have it, you can use it for small, everyday purchases (like gas or coffee) and, most importantly, pay off the balance in full every month. This creates a second track record of perfect payments.

This one-two punch tackles two critical credit score components at once: payment history and credit mix. A secured card also introduces you to another key concept in the credit world. You can learn more about this by reading our guide on what is a credit utilization ratio.

Stay Vigilant by Monitoring Your Progress

Finally, you can't improve what you don't measure. Keeping a close eye on your credit reports is non-negotiable. It’s the only way to confirm your hard work is being recognized and to watch your score climb in response to your good habits.

This vigilance also serves as your first line of defense against errors. Mistakes on credit reports happen more often than you'd think, and they can unfairly pull your score down.

Here’s a simple routine to follow:

Common Misconceptions and Potential Risks to Avoid

Taking out your first loan to help build credit is a great first step, but it's important to go in with your eyes wide open. Let's clear up a few common myths and look at the real risks so you can make this tool work for you, not against you.

The biggest mistake people make is thinking of this loan as a source of quick cash. It’s not. Unlike a personal loan where you get the money upfront, these funds are tucked away in a savings account until you've paid off the entire loan. The whole point is to build a positive payment history, not to fund a purchase.

Understanding the Real Risks

Another common trip-up is seeing a credit-builder loan as a magic wand for a low score. While it’s an incredibly effective tool, building credit is a marathon, not a sprint. You won't see a huge jump overnight; real, lasting improvement takes months of consistent, on-time payments.

The most serious risk, by far, is committing to a monthly payment you can't actually afford. The entire strategy hinges on creating a flawless track record of payments.

Before you sign anything, you have to be absolutely sure that the monthly payment fits comfortably into your budget.

Spotting Predatory Lender Red Flags

Most financial institutions offering these loans are on the level, but you still need to be careful. Predatory lenders often target people with thin or damaged credit, so learning to spot the warning signs is your best defense.

Keep an eye out for these red flags:

If you treat this loan like a serious financial commitment and vet your lender carefully, you can sidestep these pitfalls and stay on the path to a healthier credit score.

Frequently Asked Questions About Credit-Builder Loans

It's smart to ask questions before trying out any new financial tool. Let's tackle some of the most common ones about credit-builder loans so you can feel confident about your next steps.

How Quickly Will I See My Credit Score Go Up?

Building a great credit score is more of a marathon than a sprint, but you can definitely see progress sooner than you might think. Many people notice small bumps in their score within just a few months of making steady, on-time payments.

For more significant, lasting improvements, you'll want to aim for 6 to 12 months of perfect payment history. The real keys here are patience and consistency—they're your best friends on this journey.