How to Update Credit Report Quickly: Easy Steps to Improve Your Score

So, you need to get your credit report updated, and you need it done fast. The single quickest way is to go straight to the source: dispute any errors you find directly with the three major credit bureaus through their online portals.

While you have to wait for your lenders' normal reporting cycles for most positive updates (like a paid-down balance), a successful dispute can trigger a correction in as little as 30 days.

Why Credit Report Updates Take Time

It’s a classic frustration. You finally pay off a big credit card bill or clear up a negative mark, but when you check your credit report… nothing. It’s still there. This isn’t a bug in the system; it’s actually how the system is designed to work.

Think of credit reporting less like a live-streaming video and more like a monthly print magazine. It’s a massive data collection effort involving thousands of lenders and millions of people. Getting a handle on this timeline is the first step to managing your expectations and, more importantly, figuring out how to get ahead of the game.

At the end of every billing cycle, each of your creditors—your bank, your auto lender, your credit card company—bundles up your account information. They then ship that data off to the big three credit bureaus: Experian, TransUnion, and Equifax. This is the fundamental process that turns your financial actions into an official credit history.

The Standard Reporting Cycle

Most lenders report your activity—things like your current balance, payment history, and credit limit—about once every 30 to 45 days. The catch is, they don't all do it on the same day.

Your Visa card might report on the 15th of the month, while your car loan reports on the 28th. This staggered schedule is why your credit score can seem to jump around. There’s a natural delay between when you make a financial move and when it actually shows up on your report.

How Bureaus Put the Pieces Together

When the bureaus get this data from your lenders, it doesn't just get zapped into your file instantly. They have a whole process for verifying the information and making sure it gets attached to the right person. This involves sifting through huge, complex data files (often called "metro 2 tapes") to maintain accuracy.

The system is built to handle an incredible amount of information, but it wasn't built for instant speed. The main players are:

Understanding this framework is key. When you're trying to figure out how to update your credit report quickly, you’re really looking for ways to bypass this standard, slow-moving cycle.

How to Find and Document Credit Report Errors

Before you can even think about fixing your credit report, you have to play detective. You can't correct mistakes you don't know are there, and trust me, even a tiny error can do some serious damage to your score. The first move is always to get your official reports from the big three credit bureaus.

You're legally entitled to a free copy of your credit report every single week from Experian, Equifax, and TransUnion. The only place to get them safely and for free is AnnualCreditReport.com. Steer clear of other sites that dangle "free reports" but might be trying to lock you into a paid subscription.

Stick to the official source authorized by federal law. It's the best way to ensure your sensitive information stays secure. Once you have those reports in hand, the real work begins.

What to Look For

Don't just give your reports a quick glance—you need to review them line by line. It's shockingly easy for a simple typo, like a switched number in an account or a misspelled name, to create a massive headache. Treat it like you're proofreading the most important document of your life.

I’ve seen a lot of reports, and errors tend to pop up most often in these areas:

Documenting Every Error

When you find something that looks wrong, your next job is to gather the evidence to prove it. Your word alone isn't enough. I always advise people to create a dedicated folder—digital or physical, your choice—for every single error you plan to dispute.

Start collecting your proof. This could be things like bank statements showing a payment was made, a confirmation email from a creditor, or a "paid-in-full" letter. Anything that backs up your claim is crucial.

Having a basic understanding of data quality best practices can actually help you spot these kinds of inconsistencies more easily. For a more detailed breakdown of what you're looking at, our guide explaining the sections of a https://www.itinscore.com/blog/credit-report-explained/ is a great place to start.

With solid documentation in your hands, you’re no longer just making a complaint—you’re building a solid case the credit bureaus can't ignore.

Crafting a Dispute for the Fastest Results

Filing a dispute is your legal right, and honestly, it’s the most direct way to get mistakes off your credit report. But how you do it can make all the difference between a quick fix and a drawn-out headache. You’ve got a few options, but one path is clearly the fastest.

You could go old-school and mail a certified letter. This gives you a great paper trail with a return receipt, but it’s by far the slowest route. You could also try calling, which sometimes works for simple, obvious errors. The big downside? You have no clear record of the conversation, which is a huge problem if the bureau doesn't follow through.

For the quickest turnaround, your best bet is using the credit bureaus' online dispute portals. These systems are built for efficiency. They walk you through the process and let you upload your proof right then and there. This digital approach gets your case into the system almost instantly, shaving days off the timeline right from the start.

Structuring Your Dispute for Clarity

When you write your dispute, you have to be crystal clear. Simply saying "this is wrong" won't cut it. You need to be specific, professional, and straight to the point. Make it incredibly easy for the investigator on the other end to grasp the problem and see exactly what needs to be fixed.

Think of it as building a case that's too logical and well-supported for them to ignore.

To really speed things up, you have to be strategic about what you tackle first. It might be helpful to use some powerful task prioritization techniques to figure out which errors are dragging your score down the most and focus on those first.

The Power of Strong Evidence

Let's be real: your claim is only as good as the proof you can provide. Without documentation, your dispute is just your word against theirs. But when you back it up with solid evidence, it becomes a demand for action they can't easily dismiss. The proof you'll need really depends on the type of error.

Here are a few common situations I’ve seen and the kind of documents that get the job done:

Getting all your documents in order before you even start the dispute is crucial. For a deeper dive into the process, our guide on https://www.itinscore.com/blog/how-to-dispute-credit-report/ has a full walkthrough. Having everything ready to go makes the online submission a breeze and gets you that much closer to an accurate credit report.

Accelerating Updates with Advanced Tactics

When you're trying to get a loan approved or snag a low interest rate, the standard 30-day investigation window for credit disputes can feel like an eternity. The good news? You're not necessarily stuck in that slow lane.

If time is critical, there are specific, powerful strategies you can use to push for much faster updates. These aren't your everyday fixes, but in a high-stakes financial situation, they can make all the difference.

The Power of a Rapid Rescore

One of the most effective tools for a quick turnaround is the rapid rescore. The crucial thing to understand is that this isn't something you can request on your own. A mortgage lender or broker has to kick off the process for you.

Let's say you're applying for a mortgage. Your debt-to-income ratio is just a bit too high because your credit report still shows a car loan you recently paid off. Instead of waiting a month for the lender to report it, your mortgage broker can submit the payoff proof directly to the bureaus for a rapid rescore. This can get your report and score updated in just a few days, potentially saving your loan application.

This strategy is perfect for when you've made a significant positive change that just hasn't hit your report yet, like:

Going Directly to the Source

Sometimes, the quickest path is the most direct one: contacting the creditor who reported the information in the first place. If you've sorted out an issue with a lender—for instance, a payment that was wrongly marked as late—you can ask them to push an immediate, out-of-cycle update to the credit bureaus.

This is often called a "goodwill adjustment." While creditors aren't required to do it, many will, especially if the mistake was theirs or if you've been a reliable customer for years. Your success here often comes down to how you frame the conversation. We cover some great communication tactics in our guide on how to negotiate with creditors.

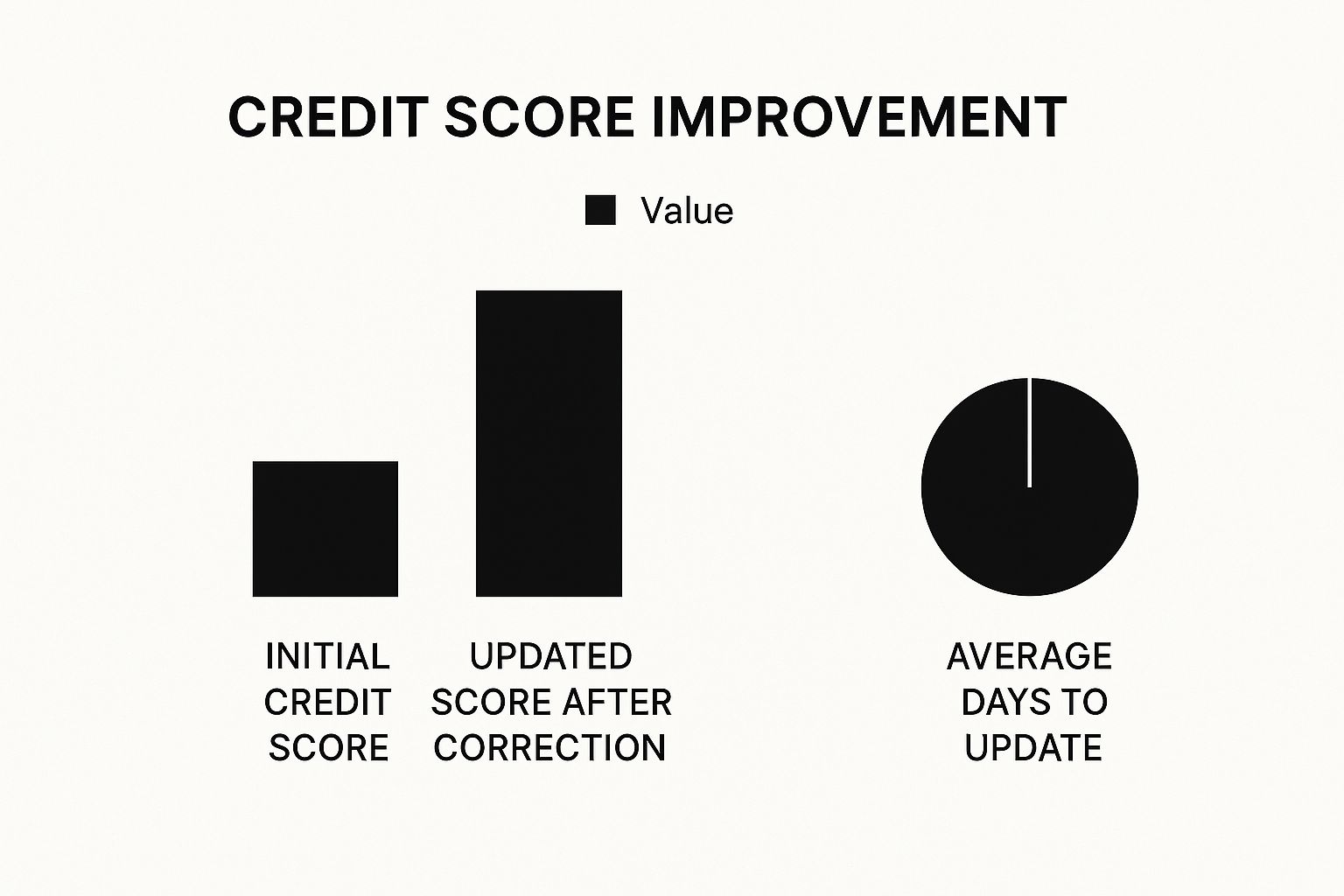

This image really drives home how much of an impact these accelerated updates can have.

It's not just about the score boost from fixing an error; it's about the massive amount of time you save by taking proactive steps.

Using Modern Tools for an Immediate Boost

The credit bureaus themselves have started offering tools that can give your score a more immediate lift. These services work by adding new, positive data to your file that wasn't being counted before.

A great example is Experian Boost™. It lets you link your bank account to get credit for on-time payments you're already making—like utilities, cell phone bills, and even streaming subscriptions. Since this payment history isn't normally reported, adding it can sometimes give your FICO® Score an instant boost. It's a smart way to build credit using your existing responsible financial habits.

To help you decide which path to take, here's a quick comparison of the different methods available.

Standard vs Accelerated Credit Update Methods

Ultimately, these advanced tactics take a bit more legwork than filing a standard dispute. But when you need your credit report to accurately reflect your financial health right now, they provide a crucial advantage. Knowing your options empowers you to take decisive action when it truly counts.

How to Confirm Your Credit Report Is Actually Fixed

Getting that "dispute complete" email from a credit bureau feels like a win, but don't pop the champagne just yet. You haven't crossed the finish line until you've seen the corrected report with your own eyes and made sure the fix is permanent. This last step is what separates a temporary fix from a lasting one.

The first piece of mail you'll get is the summary of their investigation. This is the bureau’s official verdict, and you need to read it carefully. It will tell you exactly what they decided—whether the item was deleted, updated, or if they sided with the creditor.

Reading Between the Lines of the Investigation Results

When you open that letter or email, you're looking for a few key phrases. If they say the information was "verified as accurate," that's bureau-speak for "we're keeping it." It means they believe the creditor, and the negative mark is staying put for now.

On the other hand, if you see words like "deleted" or "updated," that's a huge victory. But even then, your work isn't quite done. I've seen it happen countless times: a deleted item mysteriously reappears a few months down the road. This is called a reinsertion, and it usually happens when the original creditor accidentally sends the old, incorrect data again during their next reporting cycle.

The Only Real Proof: A Fresh Credit Report

Never, ever take the bureau's letter as the final word. The only way to be 100% sure the change was made correctly is to pull a brand-new copy of your credit report. Give it a week or so after you get the notification, then head back to AnnualCreditReport.com and grab an updated report from the specific bureau you dealt with.

Once you have the new report in hand, play detective:

What to Do If the Bureau Says No

So, what happens if your dispute is denied? First off, don't get discouraged. The bureau’s decision is far from the final say.

Your immediate next step is to look at the proof you sent. Was it as strong as it could be? Maybe a bank statement was hard to read, or a letter wasn't clear enough. Often, simply resubmitting the dispute with more powerful, undeniable evidence is enough to get the job done.

But if you've sent crystal-clear proof and the bureau or the creditor is still stonewalling you, it's time to bring in the big guns. Your next move is filing a formal complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB doesn't mess around. They'll formally forward your complaint to the company for a public response, and that official pressure is often what it takes to get stubborn errors corrected for good.

Common Questions About Fixing Your Credit Report

Even when you know the steps, real-world questions always pop up when you're trying to get your credit report updated. I've heard them all over the years. Here are some of the most common ones I get, with straight-to-the-point answers.

How Long Does It Take for Good News to Show Up?

This is probably the number one question. You’ve just paid off a massive credit card balance and you're eagerly refreshing your credit score, expecting it to soar.

The reality is, you’re on the lender’s timeline, not yours. Most creditors only send updates to the bureaus once a month, typically every 30 to 45 days. So, if your payment posts on the 5th but their reporting date isn't until the 25th, you're stuck waiting. The only real exception is a "rapid rescore," but that's a special tool only mortgage lenders can use when you're in the middle of a home loan application.