How to Get Inquiries Off My Credit Report: Easy Tips

Before you can even think about getting inquiries off your credit report, you need to know which ones you can actually challenge. The key is separating the legitimate inquiries you approved from the ones that are either inaccurate or flat-out fraudulent.

You can only dispute and remove unauthorized hard inquiries. It's a specific process: get your reports, pinpoint the questionable inquiries, and then formally dispute them with the credit bureaus.

Understanding Why Credit Inquiries Matter

Let's start at the beginning. Before you dive into cleaning up your credit report, it’s essential to understand what you're looking at and why it's so important. Not all inquiries are the same, and knowing the difference is the first real step toward taking control of your financial profile.

When you look at your credit report, you’ll see two main kinds of inquiries: "hard" and "soft." Lenders really only care about the hard ones.

The Impact of Hard Inquiries

A hard inquiry—often called a "hard pull"—is recorded when a financial institution checks your credit history because you've applied for new credit. Think credit cards, a mortgage, an auto loan, or a personal loan. Each time you apply, a formal request goes to one (or more) of the big three credit bureaus: Equifax, Experian, and TransUnion.

These formal requests can actually ding your credit score. They make up about 10% of your total FICO score. While one hard pull might just cause a small, temporary dip of a few points, a bunch of them in a short time can look like a major red flag to lenders.

From a bank's perspective, multiple recent applications might mean you're in financial trouble or about to take on way too much debt. Hard inquiries stay on your credit report for two years, though their effect on your score usually fades after the first year.

Soft Inquiries Are Different

Soft inquiries, on the other hand, don't impact your credit score at all. These happen when you check your own credit, when a company sends you a pre-approved offer without you formally applying, or when an employer does a background check. You can see them on your report, but potential lenders can't.

Since only hard inquiries affect your score and show lenders your credit-seeking activity, those are the ones you need to examine closely. For a deeper look at this, you can learn more about what a hard credit pull entails in our detailed guide.

Grasping this difference is fundamental. It lets you focus your energy on the inquiries that actually matter and stop worrying about the ones that don't.

Hard Inquiries vs Soft Inquiries At a Glance

Here’s a quick table to help you easily tell the two apart when you're looking at your report.

This foundation is crucial. With this knowledge, you can confidently sort through your credit report and identify which inquiries are legitimate and which ones might be worth disputing.

Getting Your Hands on Your Free Credit Reports

Before you can even think about disputing inquiries, you need to see exactly what lenders see. Your first mission is to get copies of all three of your credit reports—one from Equifax, one from Experian, and one from TransUnion. This isn't optional; it's the foundation of the whole process.

The U.S. government has made this part easy. The only official, truly free place to do this is AnnualCreditReport.com. Seriously, bookmark that site. Many imposter sites exist to sell you scores or sign you up for services you don't need. This is the one you want, giving you free weekly access to your reports.

The Identity Verification Gauntlet

Getting through the online verification can feel a bit like a pop quiz on your financial life. To confirm it's really you, the system will ask a series of multiple-choice questions pulled directly from your credit history. These can be surprisingly tricky.

You might see something like, "Which of the following lenders holds your auto loan opened in early 2021?" with four bank names and a "None of the above" option. Get one wrong, and you could get locked out. To avoid this frustration, I always tell people to prep a little first.

Here’s what I recommend having on hand before you start:

A few minutes of prep here will save you a major headache.

What Happens If You Get Locked Out?

It happens. Maybe you forgot about a small retail card or mistyped a previous address. If the system denies you access for security reasons, don't sweat it.

You are still legally entitled to your reports. The website will give you instructions to request them the old-fashioned way: by mail or phone. It’s slower, sure, but it’s a foolproof backup. You'll just need to send in a request form with copies of your identification.

Why Checking All Three Bureaus is Non-Negotiable

It's easy to assume that all three credit reports are identical, but that’s a common and costly mistake. Equifax, Experian, and TransUnion are competing businesses, and creditors are not required to send them all the same information.

An auto lender might only report to Experian and TransUnion. A credit card company might only report to Equifax. This means a hard inquiry you never authorized could be damaging your score with one bureau while being invisible on the others.

By reviewing all three reports side-by-side, you get the complete picture. It’s the only way to build a full inventory of every single inquiry that needs to be investigated and, potentially, removed.

Spotting Inquiries You Can Actually Remove

Alright, you've got your credit reports from all three bureaus. Now, the real detective work begins.

Not every hard inquiry you see is a target for removal. Your job is to go through that list with a fine-tooth comb, separating the legitimate inquiries you definitely made from the ones that look fishy or are flat-out wrong.

Think of it like this: a successful dispute is built on a solid foundation. You need a valid reason, like a reporting error or potential fraud, to get an inquiry removed. The inquiries from that car loan or credit card you actually applied for? Those are staying put.

Legitimate vs. Questionable Inquiries: The First Pass

The first thing to do is a high-level sort. I find it helps to print the reports out or pull them up side-by-side on a big screen. Grab a highlighter and start reading.

For every single hard inquiry, ask yourself one simple question: "Do I remember applying for something with this company around this date?"

If you get a definite "yes," that one's legitimate. Leave it alone. It’s the "no" and the "I don't think so" answers that you want to circle. This is how you start building your list of potential disputes.

By the way, you can completely ignore the soft inquiries section. While you can see them, they don't affect your credit score one bit. If you're curious, we break down why in our article about whether soft inquiries hurt your credit score.

Common Red Flags to Watch For

As you dig into your "maybe" pile, you'll start to notice some patterns. I've helped countless people clean up their reports, and these are the most common signs that an inquiry is a prime candidate for removal.

Building Your Case for Each Dispute

Once you have your final list of suspicious inquiries, it's time to build your case for each one. This doesn't mean you need a stack of paperwork. Sometimes, the evidence is simply the absence of a relationship with the creditor.

For instance, if you see an inquiry from a department store in a state you've never even been to, that’s a pretty open-and-shut case. Spot a hard pull from a mortgage lender when you've been renting for years and have never applied to buy a house? That’s a clear error.

Your goal is to have a simple, logical reason for every item you plan to dispute. This organized approach shows the credit bureaus you’re not just guessing; you're an informed consumer presenting a clear case for why your report needs to be corrected.

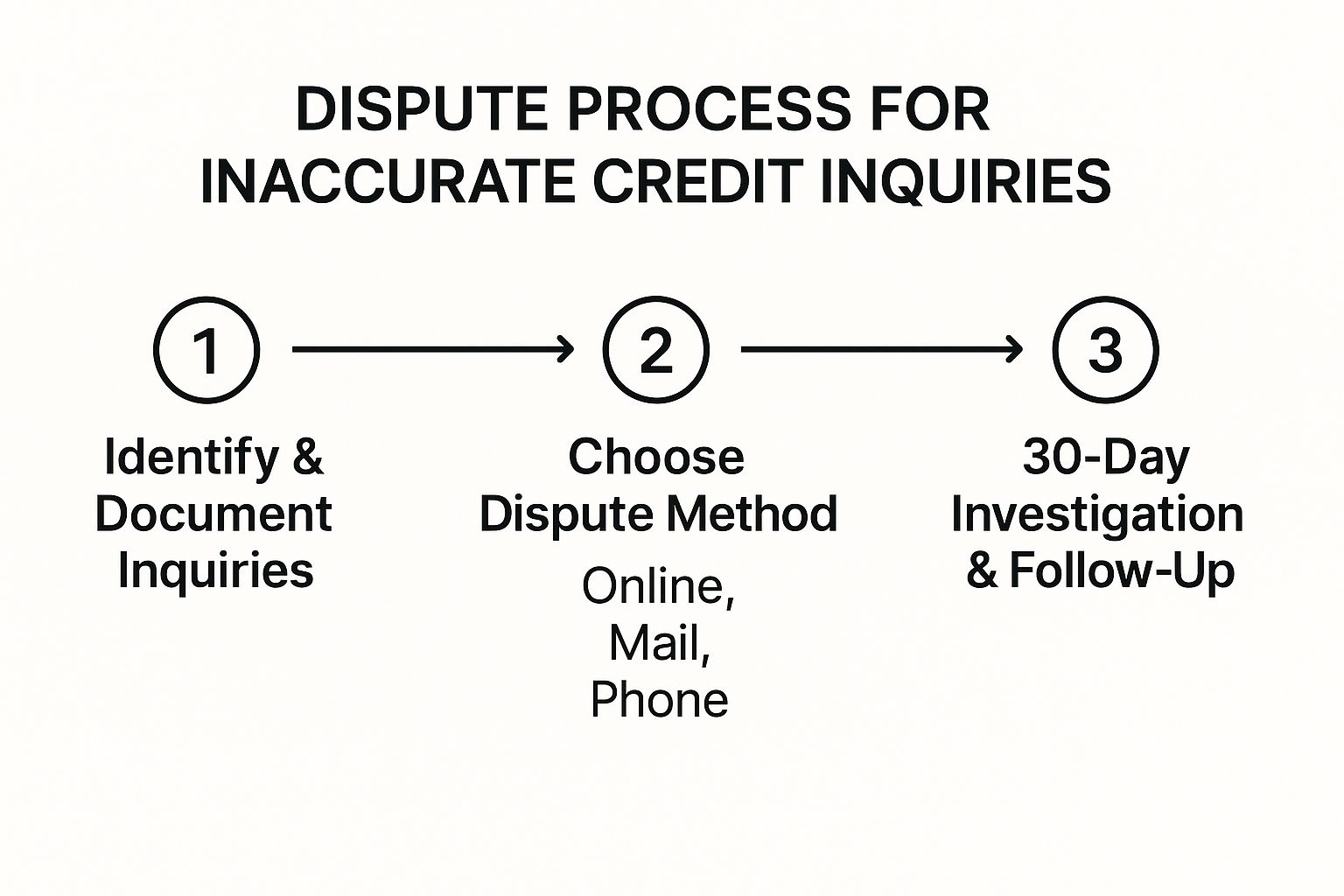

A Practical Guide to Disputing Inaccurate Inquiries

Alright, you’ve done the detective work and have a list of credit inquiries that don't look right. Now comes the part where we move from investigation to action. It's time to formally challenge those errors and get them off your credit report for good.

You have a few ways to tackle this: online, over the phone, or the old-fashioned way, by mail. While each method works, I've found that one approach consistently gives you the best results and, more importantly, the best protection.

This visual gives you a great high-level overview of the whole process.

As you can see, it's a pretty logical flow. But the devil is in the details, and that’s what we'll get into next.

Choosing Your Dispute Method

When you spot a hard inquiry you didn’t authorize—maybe from a lender you've never heard of—you have the absolute right to dispute it. These things can happen for all sorts of reasons, from a simple mix-up to a more serious case of identity theft. Your job is to act decisively.

You could jump onto the credit bureau's website or pick up the phone, and sometimes that's fine for simple fixes. But when you’re serious about getting an inquiry removed, nothing beats a formal letter sent via certified mail. It’s all about creating a paper trail. American Express has some good insights on why managing these inquiries is so crucial for your financial health.

Let's look at the options so you can see why I lean so heavily toward one particular method.

Dispute Method Comparison

Choosing how you file your dispute is a strategic decision. Each method has its own set of advantages and disadvantages, especially when it comes to creating a record of your communication.

The convenience of an online dispute is tempting, I get it. But from my experience, the best way to handle this is by sending a formal dispute letter via certified mail with a return receipt requested. Why the extra effort? Documentation. It gives you irrefutable proof that the credit bureau received your dispute and exactly when they got it.

Crafting a Powerful Dispute Letter

Your dispute letter doesn't need to be fancy legal jargon. In fact, it's better if it's not. Your goal is to be clear, concise, and professional, making it as easy as possible for the person at the bureau to understand the problem and start their investigation.

Make sure your letter hits these key points:

Following this structure gets the bureau all the information they need in one go, reducing the chance they'll kick it back for being incomplete. If you want a more in-depth guide with templates, check out our piece on how to dispute credit report errors.

The 30-Day Investigation Clock

The moment the credit bureau receives your letter, a countdown begins. The FCRA gives them 30 days to investigate your claim. They are required to contact the company that made the inquiry and ask them to prove it was legitimate.

If the creditor can't provide proof that you authorized it, the bureau must delete the inquiry. It’s the law. If they do verify it, the inquiry stays, but they have to send you the results of their investigation in writing.

This is exactly why that certified mail receipt is your best friend. It’s your proof of when that 30-day clock started ticking, and it’s how you hold the bureaus accountable.

What to Expect After You’ve Sent Your Dispute Letter

Okay, you’ve mailed your dispute letter. That's a huge step, but don't pop the champagne just yet. Now comes a waiting period, and how you handle this next phase is just as important as the letter itself.

The moment the credit bureau gets your certified letter, a 30-day clock starts ticking. Thanks to the Fair Credit Reporting Act (FCRA), they're legally required to investigate your claim within that timeframe. They'll reach out to the company that made the inquiry and ask them to prove it was legitimate. Your job now is to wait and see what they find.

Making Sense of the Investigation Results

Once their investigation is over, you'll get a letter in the mail with the final verdict. This is the moment of truth. The outcome will usually be one of three things, and you need to know what to do for each.